Why Insurance Often Doesn’t Cover GLP-1 Medications for Weight Loss (and What TRTBOSS Does Instead)

Written by

TRTBOSS Editorial Team

If you’ve looked into GLP-1 receptor agonists (and related “incretin-based” medicines) for chronic weight management, you may have run into a frustrating reality: many insurance plans won’t cover them for weight loss, even when a clinician agrees the medication could be appropriate.

This is not simply a paperwork problem. Coverage decisions for weight management medications are shaped by federal statutes, employer benefit design, pharmacy benefit manager (PBM) rules, utilization management (like prior authorization), and budget impact concerns, especially for medications with high monthly costs and rapidly rising demand.

This article explains, in plain language, why coverage is often limited, what “coverage barriers” actually mean, and how TRTBOSS is built to help patients access clinician-supervised, safety-first weight management care even when insurance says “not covered.”

Obesity is a chronic disease-yet coverage often treats it differently

Clinically, obesity is widely recognized as a chronic, relapsing, multifactorial disease that influences cardiometabolic risk, sleep, musculoskeletal pain, fertility, and quality of life. Yet in the U.S. insurance system, obesity treatment has historically been handled inconsistently-often covered for screening and counseling, but not consistently for anti-obesity pharmacotherapy.

Under the Affordable Care Act (ACA), most private plans must cover certain recommended preventive services without patient cost-sharing. Those preventive services include obesity screening and intensive behavioral interventions, as reflected by U.S. Preventive Services Task Force (USPSTF) recommendations and federal preventive-care rules.

But the ACA preventive services framework does not automatically require coverage of weight management medications.

What GLP-1 (and related incretin) medications are-at a high level

GLP-1 receptor agonists are a medication class that affects appetite regulation, gastric emptying, and glucose-related pathways. Some incretin-based therapies are FDA-approved for type 2 diabetes, while certain products in this broader category have FDA approval for chronic weight management in specific patient populations.

Evidence from large randomized trials shows meaningful average weight reduction for some patients when these medications are combined with lifestyle intervention, and some trials show cardiovascular risk reduction in selected populations.

None of this guarantees that a given person will respond, tolerate therapy, or be an appropriate candidate, and insurers often focus on cost, scope, and rules, not just clinical plausibility.

What the best evidence actually says (and what it does not)

High quality trials have demonstrated that, in appropriately selected adults with obesity/overweight, GLP-1 and related incretin therapies combined with structured lifestyle intervention can produce clinically significant average weight reduction compared with placebo.

Separate outcomes research in selected populations has also shown reductions in major adverse cardiovascular events with an incretin therapy in adults with obesity and established cardiovascular disease.

At the same time, insurers and plan sponsors often point to unanswered operational questions that matter for coverage policy, such as:

- How long does therapy need to continue for weight maintenance?

- What happens when therapy stops (weight regain risk)?

- What is the real-world adherence/tolerability profile across broad populations?

- What is the budget impact when utilization scales quickly?

These questions aren’t arguments against treatment; they’re part of why many payers implement strict controls (or exclude coverage).

Why Insurance Often Doesn’t Cover GLP-1s for Weight Loss

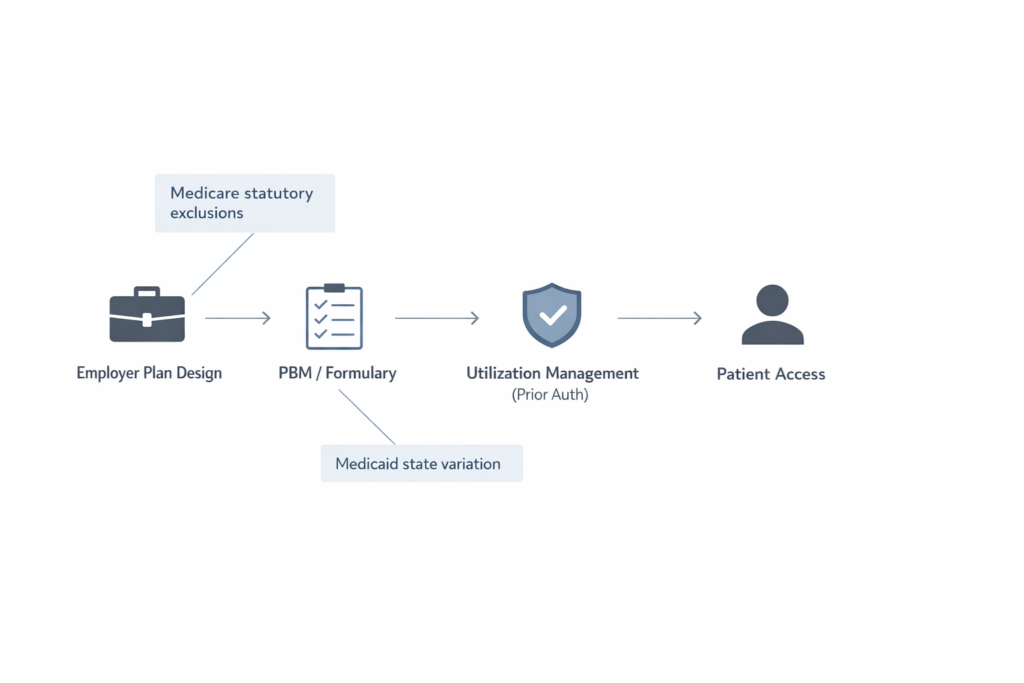

Insurance coverage decisions are usually less about “whether obesity matters” and more about how pharmacy benefits are designed and regulated.

1) Many plans explicitly exclude “weight loss medications” as a benefit category

Some health plans, especially employer-sponsored coverage, treat anti-obesity medications as optional rather than standard. Employers (or plans) may choose to exclude medications “for weight loss” while still covering the same or similar drug class for diabetes or other labeled indications.

This is a benefit design choice as much as a medical one. Many employers weigh competing priorities (premiums, total compensation, other benefits) and may decide that covering weight-loss indications is not financially sustainable at current prices and demand levels. Employer and insurer concerns about cost impact are widely reported, particularly among large firms experiencing substantial utilization.

2) Medicare has a long-standing statutory exclusion for drugs “used for…weight loss”

A key reason coverage is confusing is that Medicare Part D historically excludes drugs when used for anorexia, weight loss, or weight gain under federal statute. The Congressional Research Service (CRS) explains that even if a GLP-1 drug has FDA approval for weight loss, it is not covered under Part D when used for that purpose (with important nuance when the same medication is covered for other approved conditions, or under certain enhanced plan structures).

CMS explored policy changes in recent years, including proposals and re-evaluations tied to evolving medical consensus.

But news reporting in 2025 indicated the federal government did not proceed with a broad expansion of Medicare coverage for anti-obesity drugs at that time.

3) Medicaid coverage varies by state, and is often optional for obesity treatment

Medicaid rules differ from Medicare, and state programs have significant discretion in optional coverage categories. Recent analysis indicates Medicaid coverage for GLP-1s for obesity treatment remains limited, with a relatively small number of state Medicaid programs covering them for obesity treatment under fee-for-service as of January 2026.

Even where covered, states commonly apply utilization controls such as prior authorization.

4) “FDA-approved” doesn’t equal “covered” formularies and PBM rules still apply

Even when a medication is FDA-approved for a given use, plans can:

- Put it on a high specialty tier

- Require prior authorization

- Require documentation of clinical criteria

- Limit quantity or duration

- Require re-authorization to continue therapy

Plans also negotiate rebates and manage formularies based on net cost and contractual structures. Coverage may be available for one indication but not another, or only after specific documentation is submitted.

5) Prior authorization is often designed to slow rapid uptake

Prior authorization is frequently used when a drug is:

- High cost

- High demand

- Intended for chronic use

- At risk for off-label or non-covered indication use

Employers report significant budget impact when covering weight-loss indications, which drives tighter controls.

6) The preventive-care mandate focuses on screening/counseling, not medication coverage

The ACA preventive services requirements are real and meaningful—many plans must cover preventive services without cost-sharing, but obesity related preventive coverage is typically oriented toward screening and intensive behavioral interventions, consistent with USPSTF guidance.

That structure does not automatically convert into “coverage required” for anti-obesity medications.

7) Short-term coverage math can look “bad,” even if long-term health benefits are plausible

A major employer concern is the “wrong-pocket problem”: the employer pays now, but long-term benefits may accrue after employees change jobs or plans. Reuters reporting and employer analyses have highlighted how cost and uncertainty about long-term ROI can limit coverage expansion.

Why TRTBOSS Exists to Fill the Coverage Gap

Insurance complexity shouldn’t be a barrier to medically responsible care

When insurance does not cover GLP-1s for weight loss, patients often face a chaotic market: inconsistent access, confusing pricing, and fragmented support. TRTBOSS exists to offer a more structured path.

What TRTBOSS provides:

- Clinician-led evaluation to determine whether prescription therapy is appropriate

- Transparent cash-pay pathways designed for patients whose plans exclude weight-loss medications

- Monitoring and follow-up focused on tolerability, safety, and sustainable habits

What TRTBOSS does not do

- No “one-size-fits-all” prescribing

- No pressure to start medication if risks outweigh benefits

- No replacement of emergency care or in-person evaluation when clinically indicated

If you’re hitting an insurance wall and want a clinician to review your situation, TRTBOSS offers a structured intake and medical review so you can understand your options clearly.

Telehealth Process

What a responsible telehealth weight management pathway looks like

TRTBOSS is designed around a simple premise: patients deserve clinician-supervised, evidence-based options even when insurance coverage is inconsistent.

A safety-first telehealth workflow typically includes:

- Clinical intake & history

- Weight trajectory, prior attempts, nutrition patterns, sleep, stress, activity

- Medical history, medications, contraindications, and risk factors

- Screening for red flags that warrant in-person evaluation

- Objective data (when clinically appropriate)

- Weight, waist measures, blood pressure history

- Lab work and cardiometabolic markers based on individual risk

- Review of conditions that may change risk/benefit

- Shared decision-making

- Lifestyle foundation (nutrition quality, protein/fiber adequacy, resistance training, sleep, alcohol)

- Medication options when appropriate, including a candid discussion of side effects, monitoring, and discontinuation considerations

- Clear expectations: response varies, and there are no guaranteed outcomes

- Ongoing follow-up and monitoring

- Side effect surveillance

- Progress check-ins

- Adjustments to the plan based on tolerability and goals

Who may be considered for prescription weight management therapies (general education)

In general clinical practice, FDA-approved chronic weight management medications are often considered for adults with:

- Obesity, or

- Overweight with at least one weight-related health condition

That said, eligibility is not just about BMI. Responsible prescribing also depends on:

- Medical history and contraindications

- Medication interactions

- Pregnancy considerations

- Eating disorder screening and mental health context

- The ability to follow up and monitor safely

Safety & Risks

GLP-1 receptor agonists and related incretin therapies can be appropriate for some patients—but they are not “casual” medications. Safety-first care means understanding contraindications, side effects, and monitoring needs.

Common and clinically important risks to understand

While specifics vary by product, class-relevant safety considerations commonly include:

- Gastrointestinal effects (nausea, vomiting, diarrhea, constipation), sometimes severe

- Gallbladder disease risk signals (e.g., gallstones)

- Pancreatitis warnings/precautions (rare but serious)

- Kidney–related concerns in the setting of dehydration from severe GI symptoms

- Hypoglycemia risk primarily when combined with other glucose-lowering drugs (for patients treated for diabetes)

- Contraindications related to certain endocrine tumor histories (per prescribing information and boxed warnings for some products)

This is one reason many insurers require structured documentation: the medication decision should be individualized, not automatic.

Frequently Asked Questions

1) Why does my plan cover these medications for diabetes but not for weight loss?

Many plans distinguish coverage by FDA-labeled indication and by benefit category. A medication may be covered for one diagnosis and excluded for another, especially when the plan excludes “weight loss medications” as a category.

2) If my clinician says it’s medically necessary, doesn’t insurance have to cover it?

Not always. “Medical necessity” helps, but coverage depends on your plan’s contract terms, formulary placement, and utilization rules (prior authorization, re-authorization, step therapy).

3) Are weight-loss medications considered preventive care under the ACA?

Typically, ACA preventive requirements emphasize screening and intensive behavioral interventions for obesity rather than guaranteeing coverage of prescription weight management drugs.

4) Does Medicare cover GLP-1 medications for weight loss?

CRS explains that Medicare Part D has historically excluded drugs “used for…weight loss” from the definition of a covered Part D drug, even if FDA-approved for that use—though coverage may exist when used for other approved conditions, and policy discussions continue to evolve.

5) Why is prior authorization so common?

Plans use prior authorization to manage high-cost, high-demand therapies and to enforce coverage criteria. Employer reporting shows concerns about significant pharmacy spending impact when weight-loss GLP-1 coverage expands.

6) Are these medications safe?

They can be safe and appropriate for some patients, but they carry meaningful risks (notably GI side effects and other warnings/precautions that vary by product). They should be used only under clinician guidance with appropriate monitoring.

7) What can I do if insurance denies coverage?

Common options include confirming your plan’s weight-loss drug exclusion language, exploring prior authorization/appeal pathways if applicable, and considering transparent cash-pay care with clinician oversight. TRTBOSS can help you understand the safest and most realistic path forward without guaranteeing coverage.

8) How does TRTBOSS help when insurance won’t?

TRTBOSS is built to provide clinician-led weight management care with transparent pathways, appropriate monitoring, and structured follow-up designed for patients who are excluded by plan rules or stuck in repeated denials.

Medical Disclaimer

This content is for educational purposes only and does not constitute medical advice, diagnosis, or treatment. Decisions about medication and weight management should be made with a licensed healthcare professional who can evaluate your individual health history, risks, and goals. If you have severe symptoms (such as persistent vomiting, severe abdominal pain, chest pain, or signs of dehydration), seek urgent or emergency care.

Sources

- Congressional Research Service (CRS) — Medicare Coverage of GLP-1 Drugs (IF12758)

- https://www.congress.gov/crs-product/IF12758

- PDF: https://www.congress.gov/crs_external_products/IF/PDF/IF12758/IF12758.1.pdf

- Centers for Medicare & Medicaid Services (CMS) — Preventive Care Background (ACA preventive services)

- https://www.cms.gov/cciio/resources/fact-sheets-and-faqs/preventive-care-background

- U.S. Preventive Services Task Force (USPSTF) — Obesity in Adults: Behavioral Interventions (Sept 2018)

- https://www.uspreventiveservicestaskforce.org/uspstf/recommendation/obesity-in-adults-interventions

- KFF — Medicaid Coverage of and Spending on GLP-1s (Jan 16, 2026)

- https://www.kff.org/medicaid/medicaid-coverage-of-and-spending-on-glp-1s/

- Health System Tracker — Perspectives from employers on the costs/issues covering GLP-1s for weight loss (Oct 22, 2025)

- https://www.healthsystemtracker.org/brief/perspectives-from-employers-on-the-costs-and-issues-associated-with-covering-glp-1-agonists-for-weight-loss/

- Reuters — Rate of employers covering weight-loss drugs is flat, Cigna says (Sep 10, 2025)

- https://www.reuters.com/business/healthcare-pharmaceuticals/rate-employers-covering-weight-loss-drugs-is-flat-cigna-says-2025-09-10/

- Associated Press — Trump administration nixes plan to cover anti-obesity drugs through Medicare (Apr 4, 2025)

- https://apnews.com/article/trump-medicare-coverage-wegovy-zepbound-54bf291135fa9efec7d0ad9672c850a1

- New England Journal of Medicine (NEJM) — Once-Weekly Semaglutide in Adults with Overweight or Obesity (STEP 1)

- https://www.nejm.org/doi/full/10.1056/NEJMoa2032183

- PubMed: https://pubmed.ncbi.nlm.nih.gov/33567185/

- NEJM — Tirzepatide Once Weekly for the Treatment of Obesity (SURMOUNT-1)

- https://www.nejm.org/doi/full/10.1056/NEJMoa2206038

- PubMed: https://pubmed.ncbi.nlm.nih.gov/35658024/

- NEJM — Semaglutide and Cardiovascular Outcomes in Obesity without Diabetes (SELECT)

- https://www.nejm.org/doi/full/10.1056/NEJMoa2307563

- PubMed: https://pubmed.ncbi.nlm.nih.gov/37952131/

- FDA (Drugs@FDA label PDF) — Semaglutide injection prescribing information (Reference ID 5699541; updated label PDF)

- https://www.accessdata.fda.gov/drugsatfda_docs/label/2025/215256s023lbl.pdf

- CMS — Contract Year 2026 Policy and Technical Changes (MA/Part D) — Final Rule Fact Sheet (Apr 4, 2025)

- https://www.cms.gov/newsroom/fact-sheets/contract-year-2026-policy-and-technical-changes-medicare-advantage-program-medicare-prescription-final

- Federal Register final rule: https://www.federalregister.gov/documents/2025/04/15/2025-06008/medicare-and-medicaid-programs-contract-year-2026-policy-and-technical-changes-to-the-medicare

Frequently Asked Questions

1) Why does my plan cover these medications for diabetes but not for weight loss?

Many plans distinguish coverage by FDA-labeled indication and by benefit category. A medication may be covered for one diagnosis and excluded for another, especially when the plan excludes “weight loss medications” as a category.

2) If my clinician says it’s medically necessary, doesn’t insurance have to cover it?

Not always. “Medical necessity” helps, but coverage depends on your plan’s contract terms, formulary placement, and utilization rules (prior authorization, re-authorization, step therapy).

3) Are weight-loss medications considered preventive care under the ACA?

Typically, ACA preventive requirements emphasize screening and intensive behavioral interventions for obesity rather than guaranteeing coverage of prescription weight management drugs.

4) Does Medicare cover GLP-1 medications for weight loss?

CRS explains that Medicare Part D has historically excluded drugs “used for…weight loss” from the definition of a covered Part D drug, even if FDA-approved for that use—though coverage may exist when used for other approved conditions, and policy discussions continue to evolve.

5) Why is prior authorization so common?

Plans use prior authorization to manage high-cost, high-demand therapies and to enforce coverage criteria. Employer reporting shows concerns about significant pharmacy spending impact when weight-loss GLP-1 coverage expands.

6) Are these medications safe?

They can be safe and appropriate for some patients, but they carry meaningful risks (notably GI side effects and other warnings/precautions that vary by product). They should be used only under clinician guidance with appropriate monitoring.

7) What can I do if insurance denies coverage?

Common options include confirming your plan’s weight-loss drug exclusion language, exploring prior authorization/appeal pathways if applicable, and considering transparent cash-pay care with clinician oversight. TRTBOSS can help you understand the safest and most realistic path forward without guaranteeing coverage.

8) How does TRTBOSS help when insurance won’t?

TRTBOSS is built to provide clinician-led weight management care with transparent pathways, appropriate monitoring, and structured follow-up—designed for patients who are excluded by plan rules or stuck in repeated denials.

Select your weight management option

Tirzepatide + B12

- As low as $220/ month

- Compounded Tirzepatide (GLP-1 + GIP) + B12

- Any dose One Cost

Semaglutide + B12

- As low as $180/ month

- Compounded Semaglutide (GLP1) + B12

- Any dose One Cost

Lipotropic B12 (B12+MIC)

- Compounded vitamin injection

- Supports energy metabolism

- Bio-active B12 formula

Written by TRTBOSS Editorial Team

Related Articles

TRTBOSS Editorial Team in Sexual Health

Research Grade” vs Patient-Intended Peptides: What “Physician Use Only” Really Means (and Why Supervised Care Matters)

Introduction to Peptides Peptides are short chains of amino acids that can act as signaling molecules in the body. In clinical medicine, some peptide-based medications are regulated prescription drugs, while other peptide products exist in a gray market, often advertised online as “research grade,” “not for human consumption,” or “physician use only.” Those labels can […]

TRTBOSS Editorial Team in Blood Panel

Why Insurance Often Doesn’t Cover GLP-1 Medications for Weight Loss (and What TRTBOSS Does Instead)

Table of contents Obesity is a chronic disease-yet coverage often treats it differently What GLP-1 (and related incretin) medications are-at a high level What the best evidence actually says (and what it does not) Why Insurance Often Doesn’t Cover GLP-1s for Weight Loss 1) Many plans explicitly exclude “weight loss medications” as a benefit category […]

Felipe Gougeon, RN, MPH, BScRS-PT in Longevity

Why You Should Avoid “Research Use Only” Peptides

As a registered nurse, and a bachelor in rehabilitation sciences – physical therapy, I’ll say this plainly: when a vial says “for research use only” (RUO) or “not intended for human consumption,” that’s not marketing fluff, it’s a safety boundary. Those labels usually mean the product is being sold as a lab reagent, not as […]

Start Your Health Assessment Today

Personalized telehealth treatments tailored for you.